“Points Hacking” in Latin America 🛩

How I get $10,000+ USD in "free" travel each year...

“Travel is sooooo expensive, bro! I dunno how you can even afford it…”

I remember the first time I heard this comment after a couple years of traveling around Latin America.

I was back home for Christmas. Just visiting family and chilling with some old friends.

I laughed out loud at the comment, as thoughts of living in my $350 USD studio apartment with no air conditioning rolled through my mind.

Oh, and let’s not forget the electric shower ting’ that gave me a nice “shock” every time I got in the lukewarm water.

P.S: Cali, Colombia…what a wonderful “shithole” you are.

But once I regained my composure, I began explaining to my noob friend how traveling in LatAm was exceptionally cheap due to the low cost of living and my secret sauce…

“Points Hacking”

His jaw dropped to the floor as I explained to him how I hadn’t paid for a flight all year due to a couple of credit cards I opened up last Christmas.

While points hacking or travel hacking has been around for awhile now, many noobs still don’t use and abuse it like they should.

My noob friend was baffled, but intrigued.

What I explained to him that snowy December evening years upon years ago, I’ll break down here — with my top recommendations for travelers in Latin America specifically.

Top Recommendations

#1. Best For Travelers – Chase Sapphire Preferred® Card

#2. Best For Business Owners – Chase Ink Business Preferred® Credit Card

#3. Best For Beginners – Capital One Venture Rewards Credit Card

#4. Best For Veteran Vagabonds – The Platinum Card® from American Express

Editor’s Notes…

This is NOT financial advice. This is NOT legal advice. I’m just an autist living in Latin America who happens to travel for “free” every now and then.

This post is for US citizens only right now. I will dig deeper into “points hacking” for non-US citizens soon.

There are websites with 1,000s of articles and millions of words on this shit. There are books on the topic. This is a “barebones” guide to make things as simple as possible. But tbh, shit is really simple. Something, something about a “caveman” and such.

If you click one of my links in this article, sign up for a card, and get approved — I receive financial compensation in the form of bonus points. Irregardless of this fact, the information below is spot on and will help you travel for “free” in LatAm. But I wanted to make that clear — and cheers if you do decide to use my link when applying!

If you get a card and do NOT plan to renounce your US citizenship, then just pay that bitch off at the start of each month. The bonuses have massive value, so if you pay your card off on time — you’re going to be “in the green” — aka “making money” — aka traveling for “free” — with these. I mean shit, what I’m trying to say is: it’s worth it, as long as you don’t carry the debt for months on end.

TL:DR — Get a Chase or AMEX non-branded, i.e. not a hotel or airline card, to start. Both Chase and AMEX have great cards with huge point bonuses and valuable points.

What is Points Hacking?

Points hacking, or credit card churning, or travel hacking — whatever the fook’ you want to call it…

Well, it’s just a strategy used to maximize credit card rewards and benefits. With the idea to get “free” flights and hotel stays.

The gist of it is:

You strategically apply for and use credit cards to accumulate points, miles, or cashback, redeemable for travel or other perks.

The process involves researching credit cards with lucrative sign-up bonuses, high reward rates, and valuable perks.

“Points Hackers” meet minimum spending requirements to unlock bonuses, then move on to the next card while managing their credit scores.

They also exploit category bonuses, promotions, and referral bonuses to earn additional rewards. By meticulously tracking spending and rewards, they redeem points for maximum value, often in the form of discounted flights, travel experiences or hotel stays.

TL:DR…

You, a red-blooded male, looking to live like a king in the promised land of LatAm — can also get “free” flights and hotel stays by opening a few credit cards each year.

My Experience w/ Points Hacking in LatAm

I currently have 8 credit cards.

My credit score generally fluctuates between 710-790 throughout the course of the year:

While there’s a metric fuckton of tings’ that go into this algorithm and there’s no way in hell I’ll dig into it…

You basically get approved for a majority of cards you try to open if your score is above 700+

Once you get above 750+ or so, you get approved for like 99% of the cards you want to open.

Or at least that has been my experience.

Irregardless of your credit score, you should try to open a card or two — if “free” travel to LatAm is of interest to you.

You get a little ding on your score when they “pull your credit” or whatever, but overall:

It doesn’t hurt to try!

I try to stick with the main credit card companies when I’m opening a new card and rank them as such when it comes to “points hacking” in LatAm:

Chase

American Express

Capital One

Barclays has a few marginally average offerings and Discover is dogshit. So to start, stick with the companies above.

Personally, I tend to use 500,000-1,000,000 points per year between flights and hotels.

Over the past year, I used over 400,000+ points from ONE of my Chase cards…

Again…

That’s just *one* of the *eight* credit cards I have currently.

I fly first or business whenever I can on points, and often fly my mom down to see her granddaughter in Mexico — first class.

All for “free” or close to it.

Each card or points program values points a bit different. Again, this can get “complex” in some ways.

But general rule of thumb is…

Each point is worth between $0.005-0.02 USD.

When doing maths and shit…

100K points should give you $500-2,000 in “free” travel.

Looking into my points usage and the value of each point by program…

I get $2,500-20,000 in “free” travel every year.

I’d say $8,000-12,000 on average per year in “free” travel.

When looking at what programs and points are worth the most, I’ve personally found Chase points to be pretty damn valuable. AMEX Platinum points seem to be right up there.

Hotel program points seem to have far less value, outside of the Hyatt program. However, I’ve found Marriott points tend to go further than Hilton points.

Personal Credit Cards I Currently Use…

If you have decent credit, you absolutely MUST have a few personal credit cards to earn points.

Unless you’re either too rich to care or have a dogshit credit score, there’s legit no reason not to open 1-2 of these at minimum.

Here’s the personal credit cards I currently have…ranked:

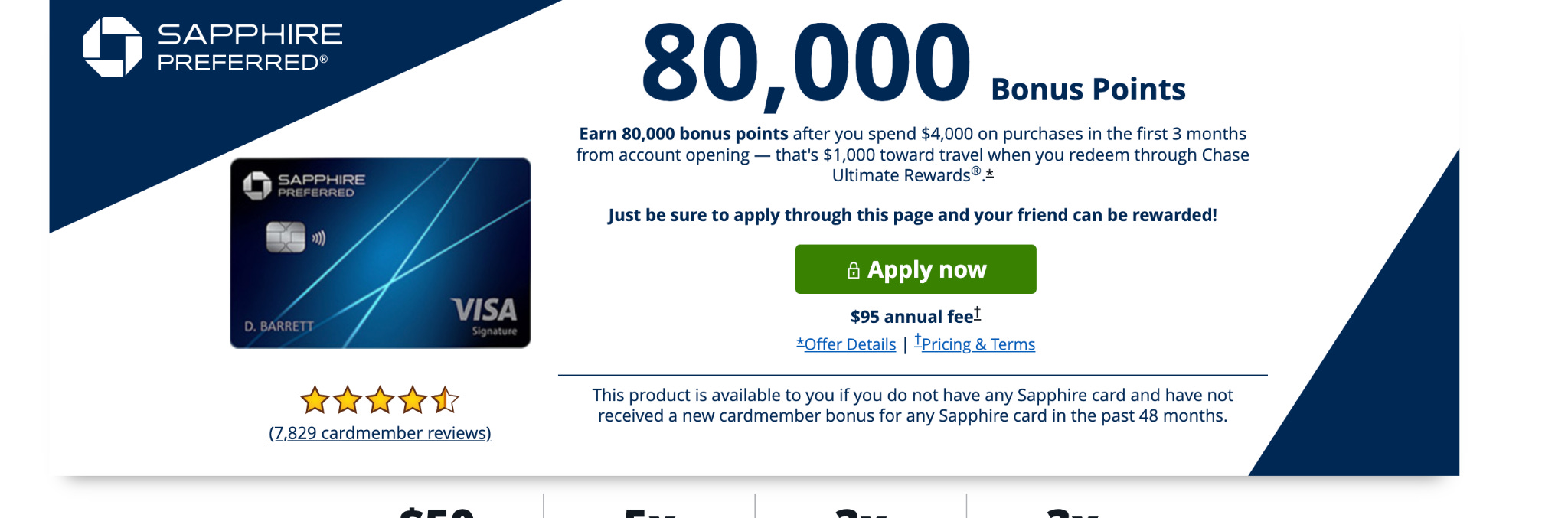

#1. Chase Sapphire Preferred® Card

Points Bonus: 80,000

Required Spend For Bonus: $4,000 in first 3 months

Annual Fee: $95 USD

Recommended Credit: Good to Excellent

Rewards Bonus Rates: 5x on travel purchased through Chase Ultimate Rewards®, 3x on dining, 2x on all other travel purchases

The Chase Sapphire Preferred® Card is a highly sought-after travel rewards credit card, offering great returns on travel and dining purchases.

Its $95 annual fee is offset by its value, with points redeemable at 1.25 cents each for travel through Chase or transferable to Chase's 14 airline and hotel partners.

Key features include earning 5 points/dollar on Chase Travel purchases, 3 points/dollar on dining, select streaming services, and online groceries, 2 points/dollar on other travel, and 1 point/dollar on everything else.

The generous sign-up bonus is valued at $1,600, and the card offers a new $50 hotel credit and premium travel protection benefits.

Overall:

If you have decent credit and want to open up one card before booking some travel to Latin America, I’d start here. Punto.

#2. Capital One Venture Rewards Credit Card

Points Bonus: 75,000

Required Spend For Bonus: $4,000 in first 3 months

Annual Fee: $95 USD

Recommended Credit: Good to Excellent

Rewards Bonus Rates: 2x miles on every purchase, 5x miles per dollar on hotels and rental cars booked through Capital One Travel

The Capital One Venture Rewards Credit Card is a solid travel rewards credit card overall.

Its $95 annual fee is well worth it, with miles redeemable for travel through Capital One or transferable to Capital One's numerous airline and hotel partners.

Key features include earning 2 miles/dollar on every purchase, making it a simple and straightforward rewards card. The sign-up bonus, valued at around $1,000 in travel, adds an additional incentive for new cardholders.

The card also comes with travel protection benefits, such as travel accident insurance, 24-hour travel assistance services, and no foreign transaction fees.

Overall:

If you have good credit and seek a versatile travel rewards card for your upcoming trip to Latin America, the Capital One Venture Rewards Credit Card is an excellent choice.

It’s not as good as the Chase Sapphire Preferred® Card, but who says you have to choose, good ser ;)

#3. The Platinum Card® from American Express

Points Bonus: 80,000

Required Spend For Bonus: $6,000 in first 6 months

Annual Fee: $695 USD

Recommended Credit: Good to Excellent

Rewards Bonus Rates: 5x points on flights booked directly with airlines or with American Express Travel, 5x points on prepaid hotels booked on amextravel.com

The Platinum Card® from American Express is a prestigious travel rewards credit card, offering exceptional benefits and rewards on flights and hotel bookings.

Its $695 annual fee is justified by the card's extensive perks, including access to over 1,300 airport lounges worldwide, airline fee credits, and hotel status upgrades. Points are redeemable for travel through American Express or transferable to their numerous airline and hotel partners.

Key features include earning 5 points/dollar on flights booked directly with airlines or through American Express Travel, and 5 points/dollar on prepaid hotels booked on amextravel.com.

The substantial sign-up bonus is valued at $1,400 or more, depending on redemption options. The card also offers premium travel protection benefits, such as trip cancellation insurance, car rental loss and damage insurance, and no foreign transaction fees.

Overall:

If you have good credit and are seeking a high-end travel rewards card with luxurious benefits, The Platinum Card® from American Express is an outstanding choice.

This is the best personal credit card for big spenders and luxury travelers.

Business Credit Cards I Currently Have…

I’m not even going to touch on some of the complexities of business credit vs. personal credit – and all that jazz.

What I will say…

If you own a company or are in any way, shape, or form self-employed:

You can open business credit cards.

The name on the card is semantics.

If you get approved, you’ll get the card. You’ll spend with the card. You’ll pay it off. You’ll get points bonuses.

Is it more complex than that?

Maybe.

But in practice, if you have tax returns showing you don’t work for someone, you can open these.

NOT financial advice.

Here’s the business credit cards I currently have…ranked:

#1. Chase Ink Business Preferred® Credit Card

Points Bonus: 100,000

Required Spend For Bonus: $15,000 in first 3 months

Annual Fee: $95 USD

Recommended Credit: Good to Excellent

Rewards Bonus Rates: 3x points on the first $150,000 spent in combined purchases on travel, shipping, advertising purchases with social media sites and search engines, and on internet, cable, and phone services each account anniversary year, 1x points on all other purchases

The Chase Ink Business Preferred® Credit Card is a top choice for business owners seeking valuable rewards on essential business expenses.

Its $95 annual fee is offset by the card's rewards potential, with points redeemable for travel through Chase Ultimate Rewards® or transferable to Chase's numerous airline and hotel partners.

Key features include earning 3 points/dollar on the first $150,000 spent in combined purchases on travel, shipping, advertising purchases with social media sites and search engines, and on internet, cable, and phone services each account anniversary year. All other purchases earn 1 point/dollar.

The generous sign-up bonus is valued at $1,250-1,750+ when redeemed through Chase Ultimate Rewards® or with various travel partners. The card also offers various travel and purchase protection benefits, such as trip cancellation insurance, primary car rental insurance, and cell phone protection.

Overall:

If you have good credit and are a business owner seeking a rewards credit card for your upcoming trip to Latin America, the Chase Ink Business Preferred® Credit Card is an excellent option.

The points bonus here is insane! But the minimum spend is high for many individuals…

#2. Capital One Spark Miles for Business

Points Bonus: 50,000

Required Spend For Bonus: $4,500 in first 3 months

Annual Fee: $0 intro for the first year, $95 after that

Recommended Credit: Good to Excellent

Rewards Bonus Rates: 2x miles on every purchase, every day

The Capital One Spark Miles for Business is a decent choice for business owners seeking a simple and valuable travel rewards credit card.

Its $95 annual fee is waived for the first year, offering an affordable option for businesses. Miles are redeemable for travel through Capital One or transferable to their numerous airline and hotel partners.

Key features include earning 2 miles/dollar on every purchase, providing a consistent rewards rate for all spending. The sign-up bonus, valued at $500-750 in travel, serves as an additional incentive for new cardholders.

The card also offers various travel and purchase protection benefits, such as free employee cards, travel and emergency assistance services, and no foreign transaction fees.

Overall:

If you have good credit and are a business owner looking for a straightforward travel rewards credit card for your upcoming travels, the Capital One Spark Miles for Business is a decent option.

The points bonus here is weak — as the number of points is smaller and Capital One points aren’t as valuable as Chase or AMEX.

Pretty easy card to open from my experience, though.

Hotel Credit Cards I Currently Have…

Hotel credit cards can be hit or miss.

Here’s why…

First off, most of my year I’m living in an apartment. So hotel points are cool and all, but they aren’t a necessity for me.

Flights, and specifically getting “free” flights, is far more important to me personally.

Second off, hotel points tend to be worth FAR less than Chase and AMEX points.

So if you have to be selective…

Go with Chase, AMEX, or even Capital One – non-hotel-branded credit cards.

On the flip-side…

For certain individuals, hotel cards are more important than anything else.

If you plan to “live” in hotels for months on end, then a hotel credit card is going to give you MASSIVE benefits.

I have a friend who used one of his hotel-branded credit cards to quickly get the highest status humanly possible at Marriott Hotels worldwide.

He lives in Marriott Hotels year-around basically — mainly in LatAm and Asia.

He gets treated like a KING the moment he walks into a Marriott anywhere in the world and the perks are solid:

Perks like…

Paying for a standard room and getting the finest suite in the place upon showing up – for no extra charge.

So yeah…

Hotel-branded credit cards have their place, especially if you love hotel living.

But for most of you grabbing a few credit cards to grab some bonuses, stick with Chase and AMEX non-hotel-branded cards.

P.S: Hotel-branded cards tend to give higher bonus points for business cards. Hence why all my hotel cards are “business” credit cards.

Here’s the hotel credit cards I currently have…ranked:

#1. Marriott Bonvoy Business® American Express Card

Points Bonus: 125,000

Required Spend For Bonus: $5,000 in first 3 months

Annual Fee: $125 USD

Recommended Credit: Good to Excellent

Rewards Bonus Rates: 6x points at hotels participating in the Marriott Bonvoy™ program, 4x points at U.S. restaurants, U.S. gas stations, and on wireless telephone services purchased directly from U.S. service providers, and 2x points on all other eligible purchases

The Marriott Bonvoy Business® American Express Card is a solid choice for “business owners” who frequently stay at Marriott properties and seek valuable rewards for their business expenses.

The card's $125 annual fee is justified by its generous rewards structure and benefits. Points are redeemable for stays at Marriott Bonvoy™ hotels or transferable to numerous airline partners.

Key features include earning 6 points/dollar at hotels participating in the Marriott Bonvoy™ program, 4 points/dollar at U.S. restaurants, U.S. gas stations, and on wireless telephone services purchased directly from U.S. service providers, and 2 points/dollar on all other eligible purchases.

The sign-up bonus, valued at over $1,100, offers additional value for new cardholders. Additional perks include an annual free night award, complimentary Silver Elite status, and premium on-property internet access.

Overall:

If you have good credit and are a “business owner” seeking a hotel rewards credit card for your upcoming trips, the Marriott Bonvoy Business® American Express Card is an option.

Great bonus for a hotel card, but definitely not a top pick — unless you’re a hotel loving traveler.

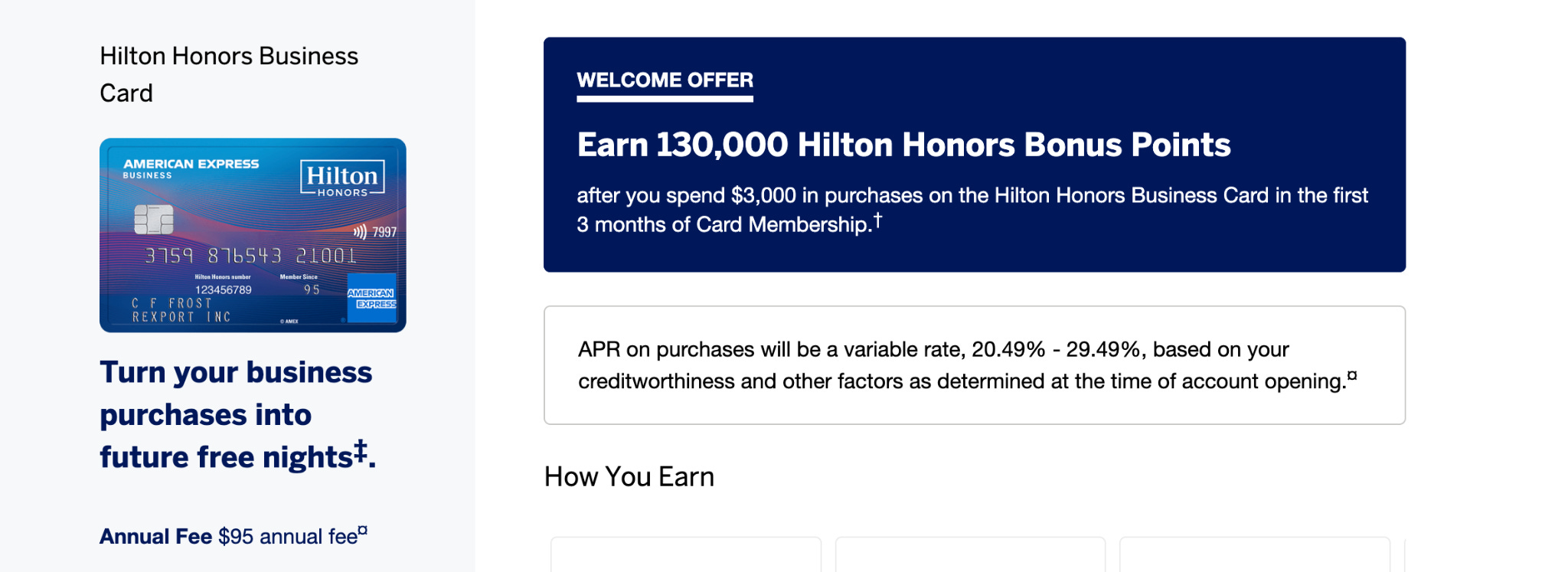

#2. Hilton Honors American Express Business Card

Points Bonus: 130,000

Required Spend For Bonus: $3,000 in first 3 months

Annual Fee: $95 USD

Recommended Credit: Good to Excellent

Rewards Bonus Rates: 12x points at hotels and resorts in the Hilton portfolio, 6x points on select business and travel purchases, and 3x points on all other eligible purchases

The Hilton Honors American Express Business Card is an option for “business owners” who frequently stay at Hilton properties and want to earn valuable rewards on their business expenses.

The card's $95 annual fee is offset by its generous rewards structure and benefits. Points are redeemable for stays at Hilton hotels or transferable to Hilton's numerous airline partners.

Key features include earning 12 points/dollar at hotels and resorts in the Hilton portfolio, 6 points/dollar on select business and travel purchases (including U.S. gas stations, U.S. restaurants, U.S. shipping, flights booked directly with airlines or through Amex Travel, and car rentals booked directly from select car rental companies), and 3 points/dollar on all other eligible purchases.

The sign-up bonus, valued at over $650, provides additional value for new cardholders. Additional perks include complimentary Hilton Honors Gold status, 10 free Priority Pass™ Select lounge visits each year, and no foreign transaction fees.

Overall:

If you have good credit and are a “business owner” who enjoys staying at Hilton properties, the Hilton Honors American Express Business Card is an option.

Just note…

Hilton points are dogshit.

Airline Credit Cards I Currently Have…

I don’t do much with airline-branded credit cards.

Here’s why:

Flexibility

Unless you know the exact routes and airlines you plan to use, these cards severely limit your flexibility when traveling.

Example…

You have 100,000 American Airlines points, but the only US-carrier that flies the route you need is United Airlines.

Doesn’t exactly help you.

Most airline-branded cards don’t do much for you while in South America or Central America, but they can help when flying back to the USA.

For example…

The one airline-branded card I do have is the:

AAdvantage® Aviator® Red World Elite Mastercard®

50,000 American Airlines miles are definitely valuable as a bonus, at least $1,000 USD in value.

But outside of flying back to the USA, these miles do you no good in LatAm.

So overall…

I’d only recommend you get an airline-branded card if you have excellent credit and have already opened preferable credit cards from Chase and AMEX.

If that’s the case, then open an airline-branded card and get a free roundtrip first-class ticket back home to see family once a year.

But there are better options out there for most of us.

“Points Hacking” w/ Latin American Airlines?

Personally…

I have never opened a credit card with a Latin American airline.

Sure, you can find cards for airlines that only fly in LatAm, like:

They pretty much all have branded credit cards these days.

I see ZERO benefit in opening one of these — unless you live in the country where they have a “hub” or whatever.

I’m confident many “points hacking” nerds have figured out a way to game this, but for 99.9% of bros traveling to LatAm…

Stick with the main US credit cards from Chase, AMEX, Capital One, etc.

Easier to get and higher points bonuses.

Sinple 🥂

Overall

If you…

Are a US citizen

Have remotely decent credit

Like to travel to LatAm

It’s a no-brainer to open up a few credit cards every year and get the points bonuses.

Those bonuses = free flights, often business or first-class, to LatAm.

And “Free” is always cool until you’re too rich to care — which hopefully we shall all be in that camp sooner than later, good ser.

But until then…

It’s a solid idea to open some of my top recommendations above, like:

Lastly, if you have any questions on points, miles, bonuses, and this whole game…

Reply to this email and I’ll do my best to break things down for you.

Ya tu sabes,

Jake Nomada